Corporate insolvencies are surging as inflation and the cost-of-living crisis continue to bite, with construction, retail and hospitality firms hardest hit – and experts don’t see this trend ending anytime soon.

Corporate bankruptcy filings began ticking up in Australia and beyond in 2023, reflecting shifting macroeconomic conditions as rising global inflation prompted central banks around the world to respond by hiking interest rates. The numbers for 2024 are even higher, with some well-known brands, particularly in more vulnerable sectors like construction, retail and travel, among the casualties.

In the construction sector, for example, major builders such as Porter Davis Homes, Probuild and Dyldam have folded in recent times. In the retail sector, a range of companies have folded, including Godfreys, Marquee Retail Group, parent company of brands including Colette by Colette Hayman, as well as The Body Shop’s UK parent, which put the future of its 100 Australian stores in doubt.

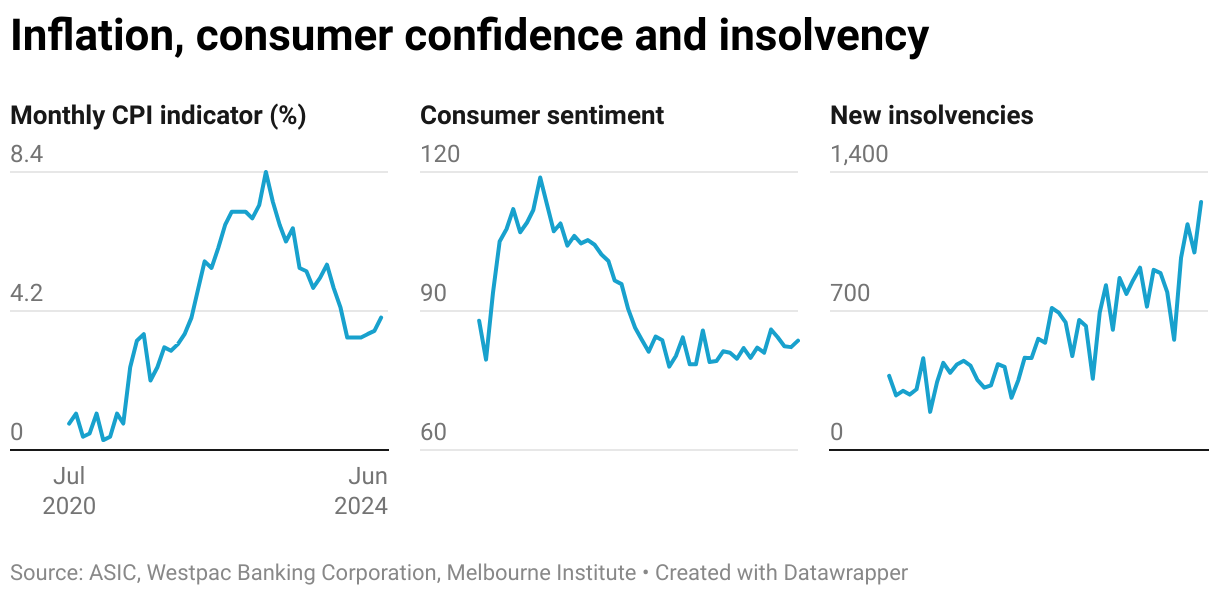

Australian companies are facing a wave of insolvencies not seen in a decade, with filings over the past 12 months topping 10,000 for the first time since 2013. This surge reflects the harsh reality of high inflation and raises concerns about a prolonged economic strain.

Data from the reveals a dramatic rise in company administrations. Filings reached 10,497 in the 2023-2024 financial year, a significant jump from 7942 the prior year. More alarmingly, these figures surpass the previous two years, when filings hovered below 5000 annually.

of this trend in April, with filings for the first nine months of the financial year already exceeding the previous corresponding period by 36.2%. Monthly filings reached 1137 insolvencies in March 2024 – a record until May, when 1249 new cases were initiated.

Inflation and debt squeeze businesses

According to Associate Professor��Evgenia Dechter, in the School of Economics at UNSW Business School, the rise in insolvency numbers is an inevitable result of economic upheaval caused by overly hot inflation that first became a global challenge in 2022.

“The present economic climate is characterised by low consumer confidence and low demand, which have a negative impact on business profitability,” says A/Prof. Dechter. “High materials costs and high interest rates, which have raised the costs associated with debt servicing, further contribute to the increase in insolvencies.”

Recent consumer price index (CPI) prints indicate high inflation is staying the course, exacerbating and threatening to further entrench these challenges. The most recent data showed monthly core inflation ticked up to 4% in May. This is the highest level this year, reflecting the fact that Australia has struggled to control rising prices compared with other developed economies.

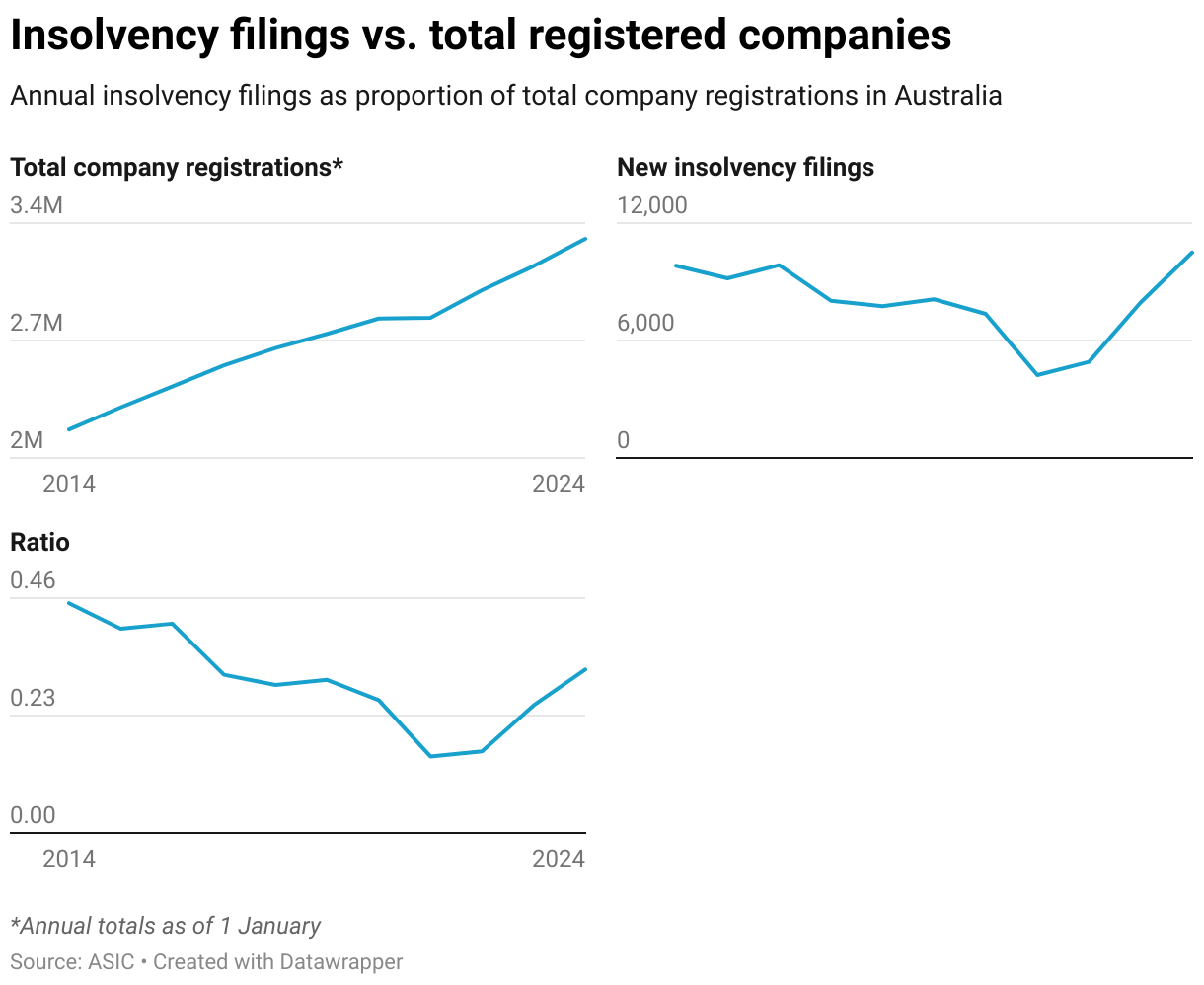

There has also been a surge in new business registrations since 2021, particularly by smaller firms with lower financial buffers, A/Prof. Dechter observes. While the insolvency figures are still concerning, ASIC also noted that due to the boost in registrations, the ratio of companies entering administration to registered companies remains lower than in 2013.

“Given that more than half of new firms close business and exit within the first three years, it’s plausible to infer that a substantial proportion of these younger and smaller entities are now exiting due to insolvency,” A/Prof. Dechter says.

“However, there is evidence that the unfavourable economic conditions also affect the more established firms,” she says.

And despite the higher base number of registered companies, the filing surge is still taking a toll, with some sectors especially exposed and a risk of flow-on effects in the supply chain.

Construction sector under pressure

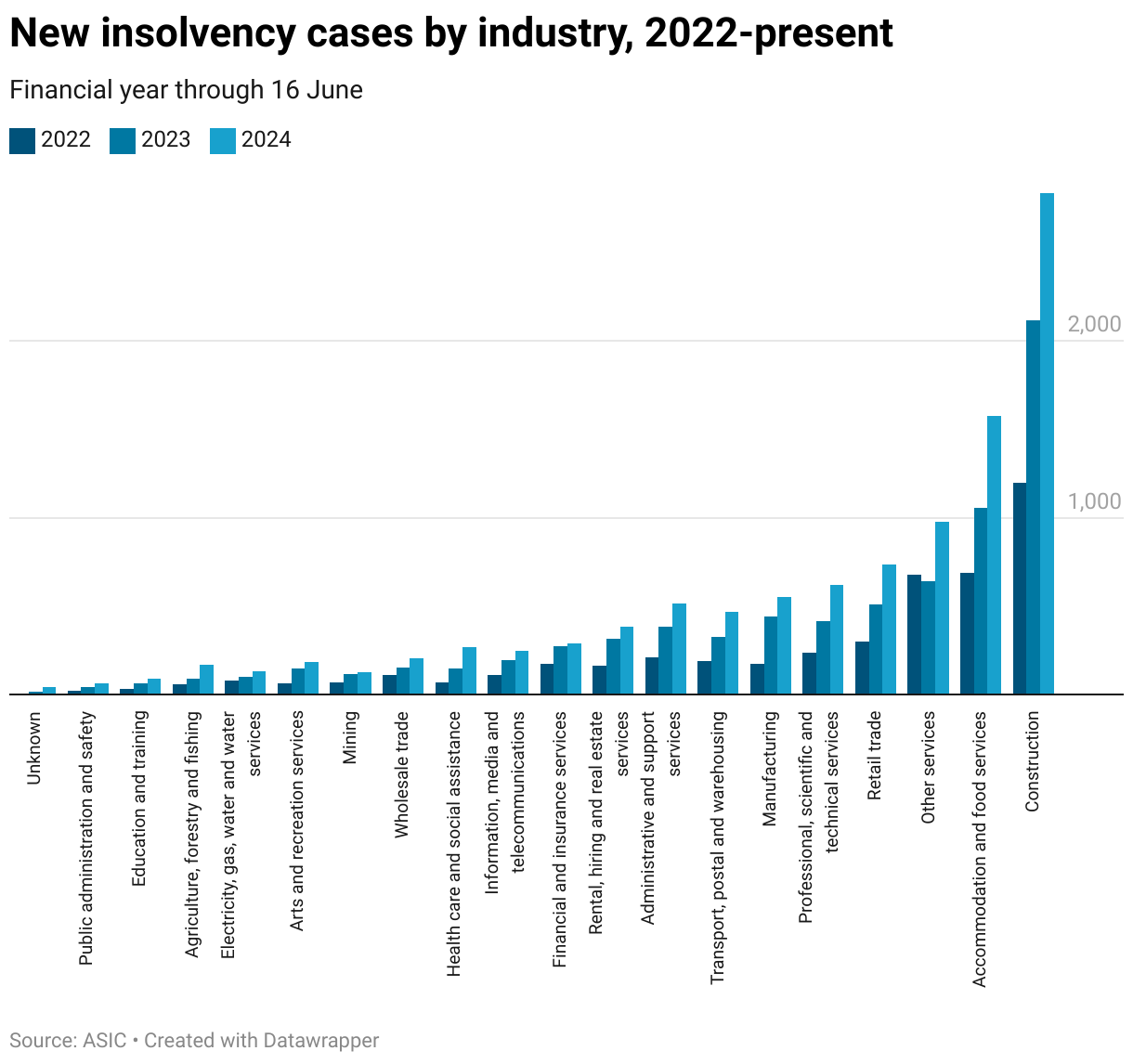

While insolvency filings have increased in all sectors, the ASIC data showed construction companies were hit hardest, with 2832 entering administration or having a controller appointed in FY 2023-2024. That’s a 28% increase from the prior year’s total of 2213, and it reflects the Australian construction sector’s exposure to pressures from high inflation and interest rates.

“The construction industry previously gained the benefits of low interest rates and stimulus policies, which led to increased demand for construction services,” A/Prof. Dechter explains. “Following the boom and entering the period of high interest rates and high building materials costs, as well as increasing labour costs, the sector became less profitable.”

According to Professor��Richard Holden, School of Economics at UNSW Business School, a key challenge for these companies is that fixed-price construction contracts are the default in Australia. When labour and materials costs increase, builders must complete the contract without adjusting the price.

“That has been a fundamental driver of a lot of these bankruptcies – if you’re forced to complete the contract and can’t renegotiate it, you can lose a lot of money,” Prof. Holden says. “That pushes a lot of people to the wall.”

Construction companies also face supply chain issues that first arose during the pandemic. All these challenges are making it more difficult for things to return to ‘normal’, and the disruption in the building sector can spread elsewhere.

“There’s been a huge shortage of construction materials and other things needed to get back into balance, to a degree,” Prof. Holden says. These supply chain issues translate to less construction and housing supply, which has a cascading effect on consumers and the broader economy.

“Anyone who’s renting has had a big rent increase, and they’re already paying more for everything else because of this high underlying inflation, and there’s less housing supply available because of how inflation has hit the construction sector,” he says. “That pushes prices up and creates a knock-on effect for a lot of consumers.”

Low consumer confidence hitting hospitality

Accommodation and food services companies are also struggling in the current economic environment, as the high cost of living prompts people to cut back while prioritising rent or mortgage payments and other necessities. A total of 1576 companies in hospitality-related sectors entered administration or had a controller appointed in the past 12 months, up from 1114 in FY 2022-2023.

“The more discretionary categories of spending tend to get cut back on, and for businesses in that sector, a large and sudden drop in demand can make it economically impossible to continue,” Prof. Holden says.

The flow-on effects of inflation and elevated interest rates also contribute to lower consumer confidence. Along with higher operational costs, this creates pressure, particularly for accommodation, food services and retail businesses, leading to a contraction in demand. ��

“These factors, compounded by the increased cost of servicing debt, have resulted in declining sales and diminished profitability within these industries,” A/Prof. Dechter says. “Cross-industry spill-over and domino effects are likely to be present as well.”

All eyes on inflation and interest rates

Like most central banks, the has been fighting to bring the inflation rate down to its target range since CPI figures began surging globally. However, the RBA has been less successful than its peers in these efforts, and Australia is one of the few advanced economies where underlying inflation has been going up in 2024 rather than coming down.

The RBA’s tool for cooling, or accelerating, inflation is the official cash rate (OCR), or the rate at which banks borrow from each other and which determines market interest rates. Before inflation started heating up, the OCR was set very low, at 0.1%, in what was then a global trend of low interest rates aimed at stimulating growth. It has now been at 4.35% – a 12-year high – since the RBA’s latest 25-basis-point increase in November.

Prof. Holden emphasises that until inflation, the cost of living and interest rates are at more sustainable levels, businesses will continue to fail at higher rates, threatening long-term economic stability.

“Our Reserve Bank has been less aggressive than other central banks in raising rates post-pandemic, a deliberate strategy to hang on to labour market gains,” he says.

“There are benefits to holding onto gains in the labour market, but there’s also the risk that inflation and interest rates stay higher for longer.”

Both academics stress the urgency of mitigating inflation and restoring consumer confidence to support economic recovery. According to Prof. Holden, one clear way to help calm inflation is to rein in the government spending that contributes to it. Instead, the latest federal and state budgets are “very expansionary”, which “just puts fuel on the inflation fire”, he says.

“If those governments want to do something to stop bankruptcies in these areas, they should stop spending so much money recklessly,” he says.

Media enquiries

For enquiries about this story or to arrange interviews, please contact, Katie Miller, News and Content Coordinator.

�ձ��:��+61 408 033 715

����������:��katie.miller1@unsw.edu.au

��